1601

Let's play the rich get everything. The rules are the rich get everything. participation is mandatory.

(lemmy.world)

Did I say mandatory? I meant optional! You're "free" to die in a cardboard box under a freeway as a market capitalist scarecrow warning to the other ants so they keep showing up to make us more!

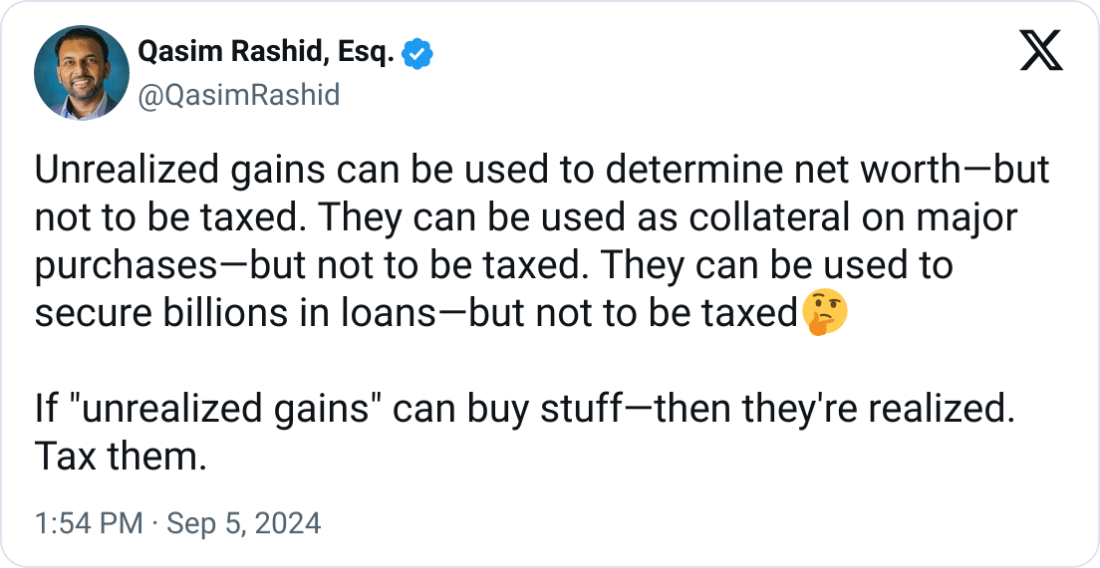

I think a law stating you can't borrow against unrealized gains would be sensible.

You can keep your unrealized gains forever, live of your dividends for all i care, and pay no tax. But realizing them, either through selling or borrowing against, triggers a taxation.

Are dividends taxed?

"Yes*"

*As with all rules, it can vary by country. As I understand it, the US tends to double tax dividends, which is a rabbit hole of why the US market chases valuation so hard

Dividends paid out to taxable accounts are taxed.

Dividends that pay into non-taxable accounts can accumulate until they are withdrawn.

So, for instance, if you own $100 of Exxon in a regular brokerage account and $100 in an IRA, the $5 dividend you get from the first account is taxable but the $5 from the second is not.

This gets us to the idea of Trusts, Hedge Funds, and other tax-deferred vehicles. If you give $100 to a Hedge fund and it buys a stock in the fund that pays dividends, it never pays you the dividend on the stock so you never have to realize the dividend gain. You simply own "$100 worth of Citadel Investments" which becomes "$105 worth of Citadel Investments" when the dividend arrives.

I think dividends in a tax-exempt accounts, like a traditional IRA, are only not taxed if you reinvest the dividend or just leave it in your brokerage account. If you move money from your IRA account to, say, your checking account, that's when you pay taxes (and there are generally fees for moving money out of tax exempt accounts without meeting certain conditions, like being of retirement age).

Right. Although, with a ROTH IRA, you pay taxes before you put the money in. Then you earn tax free even after you take it out. That makes it the preferable vehicle for long-term savings (you should expect your initial investment to double every 10 years, assuming a 7% ROI which is fairly modest - so over 30-40 years you're saving 8x on the eventual withdrawal).

But this isn't just limited to IRAs. Using investment funds, you can pull the same trick. Buy the fund, then allow the broker to shuffle the investments within the fund as they please. You only "earn" the money when you exit the fund, in the same way you only "earn" your retirement when you withdraw from your IRA.

Savings accounts and trusts can then be structured to be inheritable tax-free, with your heirs having access to withdraw from the fund without ever actually owning the money (and thus needing to pay taxes on the inheritance). And to make it even more squirrelly, you can borrow against these funds, which allows you to make large purchases without ever actually spending any money. This maneuver, plus a cagey use of declared loses, means you can avoid paying any tax on any investment income virtually indefinitely.

There is a big maybe on whether Roth is better than traditional IRA/401k.

My kids are at the age where they are making those bets now. So I made a hugely complicated forecasting tool to forecast which would be better.

I think it really comes down to your view on future tax rates.

Your mileage may vary.

Unless you're banking on a 0% tax, the ROTH is hard to beat. Compound that by the Traditional IRA being taxed at the normal rate rather than the capital gains rate, and there's very little reason to use it unless you're really bullish on tax cuts in the long term.

Thanks for expanding on the finer points! With inheritance, they also reset the cost-basis when the owner dies, which means that all the capital gains accumulated over the time that the deceased had ownership is never taxed. Like, if I bought stock for $10, die when it's worth $100, my sister inherits it, and then sells it for $110 a while later, she only pays capital gains on $10 -- not $100.

I don't think people fully realize how dramatically our tax code rewards capital, at the expense of labor, not just in the broad-strokes (like the tax rate for capital gains vs the rates for income tax brakets) but also in these little details that are easy to overlook. So thanks for the discussion!

I largely agree with all the points made here however I think the overall message is a bit misleading. I would disagree that Roth investments are the preferred for long term investments. You aren't accounting for the opportunity cost of the taxes paid in the initial investment year. Those taxes, while small compared to what you will withdraw tax free are also losing out on 8x-ing themselves (as you would have invested that amount in a traditional tax advantaged account).

What this means is Roth is the preferable savings method if you are in a lower marginal tax rate than you expect to be in retirement. However traditional is better if you are in a higher marginal rate than you expect to be in retirement. If the marginal tax rate was the same when you invest and retire then the difference between Roth and traditional would be nil.

If you're maxing out your contributions, it won't matter, except in so far as what you can earn on taxed income outside of the IRA account. That's going to be marginal relative to the contribution. And the compound returns inside the IRA make it meaningless.

Unless you're going straight into a white shoe law firm or extraordinary paying tech job after you graduate, that's pretty much everyone. But even folks going into Fortune 500 companies typically start in the $60-80k/year range and climb up from there.

The amount of money you have in the fund is going to be much larger.

Say I invest $5000/year up front and get a 10% return for 40 years. I'm looking at putting in $200,000 over that time and taking out $2.2M.

Assuming the tax rate is 25% for each of those years, I paid $50k in taxes to invest that initial $200k. But I get the $2.2M back tax-free.

If I put the $200k in tax-deferred, I have to pay $550k to get my balance out again.

Now, we can argue that I could put the $400/year in deferred taxes into a taxable savings account. And maybe we get clever by shielding that investment from taxation annually because we just shove it all in Microsoft or Berkshire B and let it ride. That nets me another $177k over 40 years, assuming the same rate of return (for which I'm still on the hook at 15% long term gains rate - so really only $150k).

The ROTH is $350k better. That's the whole reason the fund exists. It's another accounting gimmick to give wealthy people a stealth tax cut. Only suckers put their money in Trad IRAs.

You seem to be using many different assumptions separately. In the first you assume you are maxing a Roth IRA (in my initial response I was also considering 401ks as many of them have Roth options nowadays). If you are maxing your Roth 401k and Roth IRA you are likely a high earner and therefore likely in a higher tax bracket than you will be in retirement. This means that kind of person will likely prefer traditional investments.

Your assumption there is someone maxing out their retirement options and in a relatively low tax bracket doesn't seem like reality. So in your math example they wouldn't be putting the extra in a taxable brokerage account but in the same tax advantaged account.

Quick edit: also I'm confused on the extra $400/year into taxable account. It should be $1,250 per year (25% of the 5,000) which would be closer to $600,000 before the capital gains tax.

Yes

Not sure if it's the same everywhere, but if I pull a dividend I don't pay tax initially, but when I do my income taxes it's part of my income and I'd have to pay tax on it then

Careful with that. If you're not making estimated tax payments on your dividends (or other capital gains) every quarter or increasing your withholdings from wages to compensate, and you owe too much at the end of the year, you can get hit with penalties and interest.

For most people the quarterly dividends in their brokerage aren't enough to trigger that, but as your savings grows and quarterly dividends become significant they might.

Where I'm from, we don't do that. All dividends come with an "imputation credit," which basically says "this money's already been taxed."

Mhm. There's two very good reason unrealized gains aren't taxed: volatility and cash flow. Are you and the government expected to swap cash back and forth everyday to correct for changes in the market? No that's silly. Should people go into debt because they don't have the cash to pay the taxes of a baseball card they happen to own that is suddenly worth millions? Also silly.

For that same reason, using unrealized gains as security is dangerous, just like the subprime loans market was!

if you secure debt against them, they should be taxed?

Yeah owning a baseball card worth money sure whatever, if you pawn that card sorry, pay taxes. You use that card a to secure a loan with lower interest rates than you'd get without then sorry, you are realizing gains whether or not you want to admit it. This goes along one of the lawsuits against Trump. He lied to get favorable interest rates by overvaluing his assets to get better interest rates. If that's against the law why the fuck is that not counted as a "gain" to use assets to secure favorable interest rates?

There's a very good reason they should be taxed; half a dozen people are richer than god, and basically never pay any real amount of tax.

This would effectively lock out every small investor from the stock market due to the liability of both success and failure.

How so?

"Oh no, I made money, better put a small percentage of my gains away for tax season, just like I do with all of my income, because I'm American and lack a good PAYE system".

No it wouldn't. The proposal out there right now has a floor of something like a million dollars. Most of us will never need to worry about that.

I mean the stock market is literally gambling, so the risk of success and failure is already there. The proposal is whether or not we should allow people to use unrealized gains to secure loans without having to pay taxes on said gains at the point of taking the loan. This would only occur if you're worth more than 100 million. You can afford to pay that tax.

We're talking about the stock market. And it would be quarterly or annual. Please stop exaggerating.

There's a precise moment in time you take a loan. Use that moment in time to calculate worth; tax.

Sure, but this shouldn’t apply to everybody. Unrealized gains up to $10 million don’t get taxed. Unrealized gains over that amount get taxed.

If you pay it yearly you’re not paying this every day. People with this much money almost always go up in unrealized gains every year, so it’s not going to be a back and forth. It’ll be a yearly adjustment. No different than literally everybody else that pays taxes on their new wealth every year.

Edit: as for the baseball card example, if you’ve got over $10 million in unrealized gains on baseball cards, yeah, maybe you pay taxes on that.

That was my thoughts as well.

Or doing so, it counts the loan as income and is taxed accordingly. But seriously, the main aim itself can also be taxed. A house is...

Wouldn't that affect things like Home Equity loans?

Homes are taxed based on assessed value. They are already a form of taxing unrealized gains.

Most of the population either has:

I think it's fair to ask that the rich play by the same rules. You can either borrow against your gains and pay taxes on them, or not pay taxes and not be able to borrow against them.

No because the mínimum for this to apply is 100 million.

The government also told the public that the income tax was going to apply only to rich people, how'd that turn out?

Depends on the exact implementation, but sure, you could happily write a version where an initial home loan isn't hit, and only "top up" loans against the INCREASED value of your home is targeted.

How are you going to enforce that? The Bank can cite whatever they want for giving the loan.

If we just tax them then it's easily enforceable and it's done.