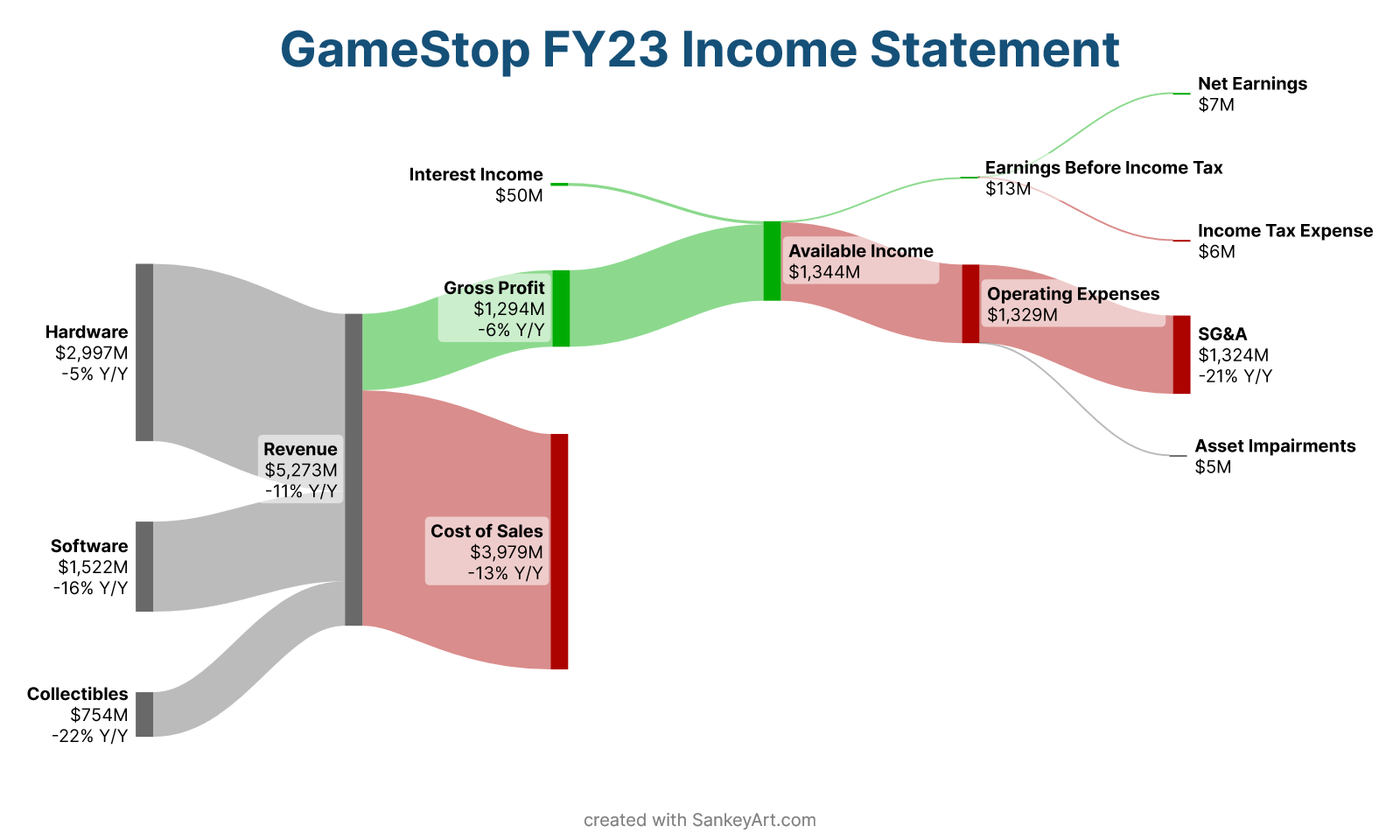

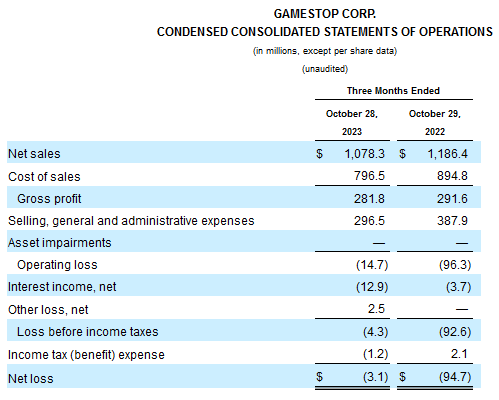

Operating loss of $35 M (compared with operating loss of $312 M in FY22)

Small but notable net earnings of $6.7 M (compared with net loss of $313 M in FY22)

How did GameStop make $50 million in interest income?

Operating loss of $35 M (compared with operating loss of $312 M in FY22)

Small but notable net earnings of $6.7 M (compared with net loss of $313 M in FY22)

How did GameStop make $50 million in interest income?

GameStop reported full-year profitability for fiscal year 2023, contradicting the prevailing media sentiment that GameStop is a terrible company destined for bankruptcy

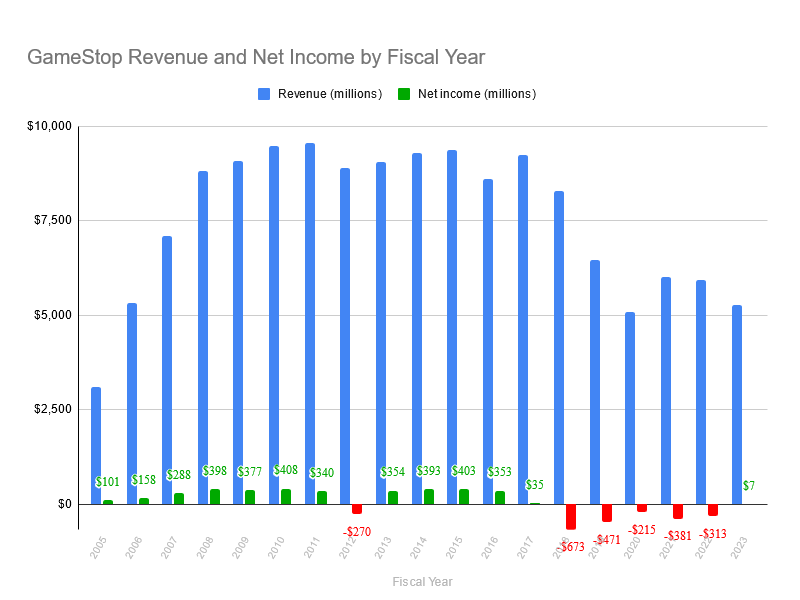

From a historical point of view, GameStop was consistently profitable every fiscal year from 2005 through 2016, with the exception of 2012. Starting in fiscal year 2017, GameStop began showing reduced profitability, and from FY 2018 through FY 2022, was unprofitable.

Source: GameStop 10-K filings - Google Sheets

Looking exclusively at revenue, it is clear that there has been a significant reduction starting approximately with fiscal year 2019. Much of this can be attributed to the fact that gamers are increasingly buying games digitally rather than in the form of physical discs such as can be purchased at a brick-and-mortar retail store like GameStop.

Yet, even in fiscal years 2017 and 2018, it is clear that despite high revenues the company was not performing well.

Heading through 2020, GameStop was undeniably a struggling company facing significant challenges, and according to many was destined for bankruptcy. The trading price of GME reflected this prevailing sentiment, and the financial media was dutifully critical.

In 2020, activist investor Ryan Cohen began purchasing shares of GME, ultimately becoming the largest individual owner of the company with approximately 12% ownership. By June 2021, the entire board of directors of the company was replaced by Ryan Cohen and his associates, with Ryan Cohen becoming chairman of the board. From this time onward, control of the company was completely in the hands of this new leadership team.

"We inherited a bunch of legacy everything, and under-investment across the entire business –- people, the entire technology stack, just decades of neglect, and so it’s hard to turn around a brick and mortar retailer that’s under the kind of pressure that GameStop was and continues to be under, but that was also part of the attraction going into GameStop was that a transformation the likes of GameStop was really unprecedented and I was motivated by that."

The company went from a situation where it was losing hundreds of millions of dollars per year to net profitability in fiscal year 2023.

While this is an undeniably positive result for the company in this time period, GameStop continues to face numerous challenges and must continue to improve and adapt in order to successfully compete in the modern video game industry.

What does mainstream financial media have to say about GameStop achieving full-year profitability for the first time in 6 years?

GameStop faces 'unsustainable' sales decline, cuts jobs to control costs

GameStop Q4 Earnings Highlights: Retail Favorite Stock Plunges After Revenue, EPS Miss

GameStop Stock Plummets Following Q4: Profitability Fails to Offset Significant Revenue Miss

GameStop Stock Plunges After Earnings Fall Short of Expectations—Key Level to Watch

Jim Cramer Says GameStop Is Arguably The Worst Company In America

GameStop could be gone in less than 5 years, says analyst

GameStop Needs To Get Its Game Back

GameStop Confirms More Layoffs, Share Price Tumbles After Sales Slide

A Sales Slump Is the Kiss of Death for GameStop Stock

GameStop saga ends. Winner: capital markets

GameStop Stock: Is This The End of a Saga Or Just Another Chapter?

Searching for recent news about GameStop yields mostly negative sentiment that fails to even mention at all that GameStop achieved full-year profitability for the first time in 6 years.

Failing to mention this important detail is a deliberate decision that reveals a clear bias in the media. It goes beyond just reporting about true negative facts about GameStop. It demonstrates a deliberate effort, by those culpable writers and media outlets, to propagate a specific sentiment about the company that is not allowed to even mention contextually important true positive facts about the company.

GameStop was profitable for the first time in 6 years - this is the news headline that captures the significance of GameStop's recent earnings report. Yet, an unassuming person who consumes mainstream financial media likely would not even learn about this important fact at all.

Who would benefit from that?

Why are there competing, mutually exclusive narratives?

There are competing narratives because there are competing financial interests.

One of the listed news articles, GameStop saga ends. Winner: capital markets, from Reuters, draws some attention to this ongoing conflict while declaring that the conflict is actually over and one side has won and one side has lost.

GME shareholders that believe in the company turnaround and leadership, despite the real challenges faced by GameStop, have a vested financial interest in the success of the company, with a desire for the share price of GME to go up, and naturally will promote the narrative that supports this financial interest.

In opposition to GME shareholders are all of the financial market participants that have a vested financial interest in the share price of GME going down. An example of such a participant would be any hedge fund that has a net short position on GME. The article refers to this faction as "shorts", recogonizing that such a faction with an interest does exist. Naturally, members of this faction will promote the narrative that supports their financial interest.

If the prospect of GameStop's success was not an ongoing threat to one faction of incumbent market participants, then there would be no reason to deliberately omit the fact of GameStop's profitability, to pretend that it isn't something that even happened at all.

Recognizing that there is an ongoing financial competition between factions that stand to benefit financially from a particular outcome of the GME share price, which faction benefits when most mainstream financial media articles propagate negative sentiment about GameStop and deliberately ignore the contextually significant fact that GameStop was profitable?

It is clear: much of mainstream financial media is actively propagating biased narratives to the benefit of the faction that has a vested financial interest in the share price of GME going down.

An interactive version of this article can be found at gmetimeline.org/fy23-profitability

For the first 3 quarters of FY 2023, GameStop has posted a total net loss of $56.4 million.

Therefore, in order to achieve full-year profitability, GameStop must achieve greater than $56.4 million in net profit for Q4 2023.

This is certainly achievable, though not guaranteed.

Something like a $100 million net gain for Q4 is possible, but not necessarily very likely.

Therefore, in any case of full-year profitability, at best, the PE ratio for GME will almost certainly be above 100, but will more likely be in the several hundreds, or worse.

By comparison, the average PE ratio for S&P500 is around 25.

https://www.macrotrends.net/2577/sp-500-pe-ratio-price-to-earnings-chart

Some PE ratios of other companies:

TLDR: Full-year profitability will be a momentous achievement, but in almost all cases, GME would have a very high PE ratio. Over the following quarters / years, GameStop will still need to increase profits substantially in order to obtain a good PE ratio.

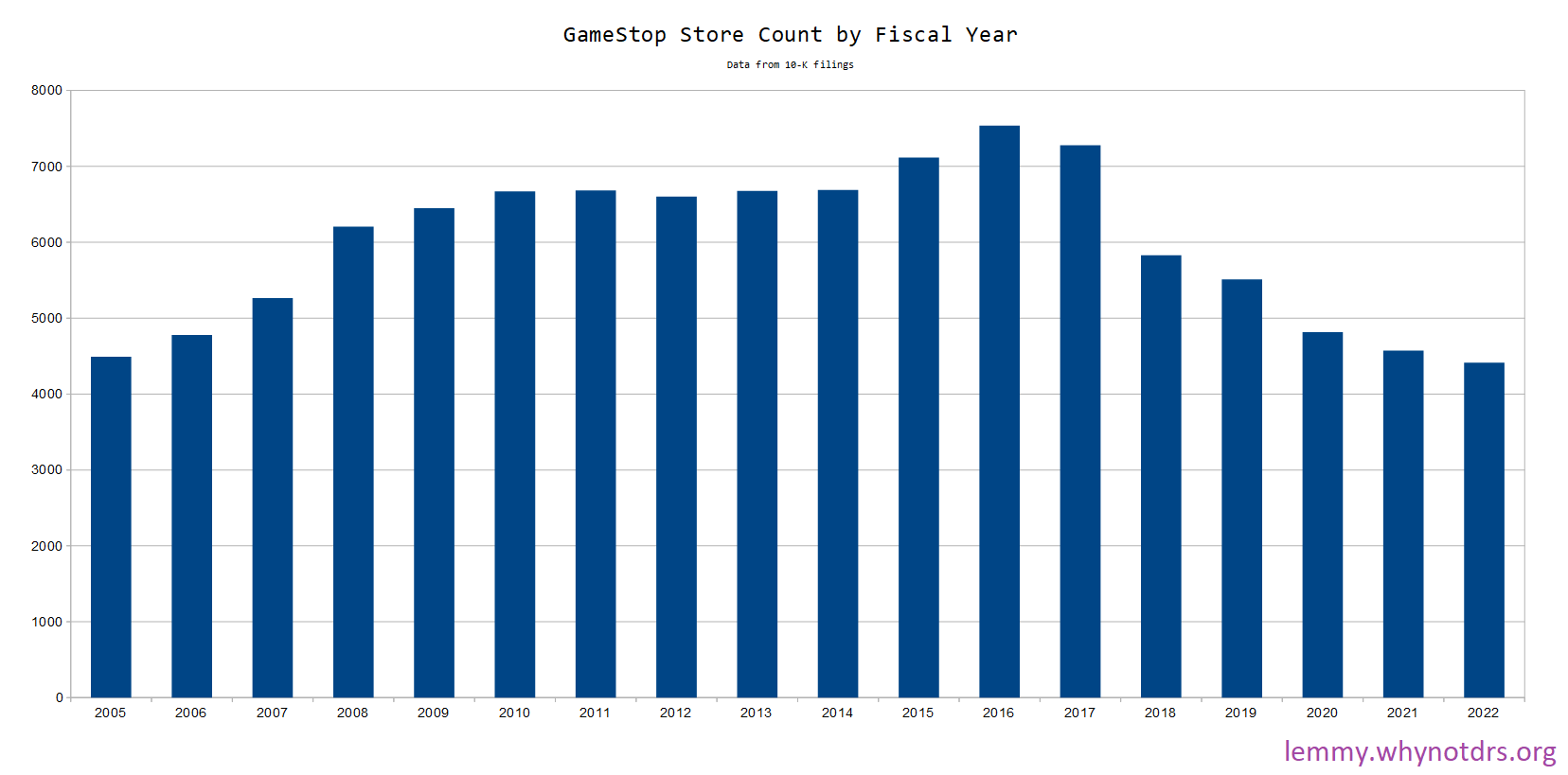

Breakdown of GameStop stores by Technology Brands stores versus Video Game Brands stores versus all International stores

And for fun,

GameStop Net Income Per Store

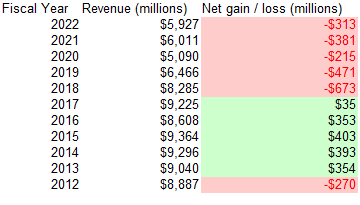

| Fiscal Year | Revenue | Net Income | Store Count | Revenue Per Store | Net Income Per Store | 10-K |

|---|---|---|---|---|---|---|

| 2005 | $3,091,783,000 | $100,784,000 | 4490 | $688,593.10 | $22,446.33 | link |

| 2006 | $5,318,900,000 | $158,250,000 | 4778 | $1,113,206.36 | $33,120.55 | link |

| 2007 | $7,093,962,000 | $288,291,000 | 5264 | $1,347,637.16 | $54,766.53 | link |

| 2008 | $8,805,897,000 | $398,282,000 | 6207 | $1,418,704.20 | $64,166.59 | link |

| 2009 | $9,077,997,000 | $377,265,000 | 6450 | $1,407,441.40 | $58,490.70 | link |

| 2010 | $9,473,700,000 | $408,000,000 | 6670 | $1,420,344.83 | $61,169.42 | link |

| 2011 | $9,550,500,000 | $339,900,000 | 6683 | $1,429,073.77 | $50,860.39 | link |

| 2012 | $8,886,700,000 | -$269,700,000 | 6602 | $1,346,061.80 | $40,851.26 | link |

| 2013 | $9,039,500,000 | $354,200,000 | 6675 | $1,354,232.21 | $53,063.67 | link |

| 2014 | $9,296,000,000 | $393,100,000 | 6690 | $1,389,536.62 | $58,759.34 | link |

| 2015 | $9,363,800,000 | $402,800,000 | 7117 | $1,315,694.82 | $56,596.88 | link |

| 2016 | $8,607,900,000 | $353,200,000 | 7535 | $1,142,388.85 | $46,874.59 | link |

| 2017 | $9,224,600,000 | $34,700,000 | 7276 | $1,267,811.98 | $4,769.10 | link |

| 2018 | $8,285,300,000 | -$673,000,000 | 5830 | $1,421,149.23 | $115,437.39 | link |

| 2019 | $6,466,000,000 | -$470,900,000 | 5509 | $1,173,715.74 | $85,478.31 | link |

| 2020 | $5,089,800,000 | -$215,300,000 | 4816 | $1,056,852.16 | $44,705.15 | link |

| 2021 | $6,010,700,000 | -$381,300,000 | 4573 | $1,314,388.80 | $83,380.71 | link |

| 2022 | $5,927,200,000 | -$313,100,000 | 4413 | $1,343,122.59 | $70,949.47 | link |

| Fiscal Year | Revenue | Net Income | Store Count | Revenue Per Store | Net Income Per Store | 10-K |

|---|---|---|---|---|---|---|

| 2005 | $3,091,783,000 | $100,784,000 | 4490 | $688,593.10 | $22,446.33 | link |

| 2006 | $5,318,900,000 | $158,250,000 | 4778 | $1,113,206.36 | $33,120.55 | link |

| 2007 | $7,093,962,000 | $288,291,000 | 5264 | $1,347,637.16 | $54,766.53 | link |

| 2008 | $8,805,897,000 | $398,282,000 | 6207 | $1,418,704.20 | $64,166.59 | link |

| 2009 | $9,077,997,000 | $377,265,000 | 6450 | $1,407,441.40 | $58,490.70 | link |

| 2010 | $9,473,700,000 | $408,000,000 | 6670 | $1,420,344.83 | $61,169.42 | link |

| 2011 | $9,550,500,000 | $339,900,000 | 6683 | $1,429,073.77 | $50,860.39 | link |

| 2012 | $8,886,700,000 | -$269,700,000 | 6602 | $1,346,061.80 | $40,851.26 | link |

| 2013 | $9,039,500,000 | $354,200,000 | 6675 | $1,354,232.21 | $53,063.67 | link |

| 2014 | $9,296,000,000 | $393,100,000 | 6690 | $1,389,536.62 | $58,759.34 | link |

| 2015 | $9,363,800,000 | $402,800,000 | 7117 | $1,315,694.82 | $56,596.88 | link |

| 2016 | $8,607,900,000 | $353,200,000 | 7535 | $1,142,388.85 | $46,874.59 | link |

| 2017 | $9,224,600,000 | $34,700,000 | 7276 | $1,267,811.98 | $4,769.10 | link |

| 2018 | $8,285,300,000 | -$673,000,000 | 5830 | $1,421,149.23 | $115,437.39 | link |

| 2019 | $6,466,000,000 | -$470,900,000 | 5509 | $1,173,715.74 | $85,478.31 | link |

| 2020 | $5,089,800,000 | -$215,300,000 | 4816 | $1,056,852.16 | $44,705.15 | link |

| 2021 | $6,010,700,000 | -$381,300,000 | 4573 | $1,314,388.80 | $83,380.71 | link |

| 2022 | $5,927,200,000 | -$313,100,000 | 4413 | $1,343,122.59 | $70,949.47 | link |

nice post OP! love your original art.

it often takes me a while to figure out what it says when looking at the static images. this one took me a solid 2 minutes.

TERMINATE DSPP!

Another example, January 29, 2024.

Why do they do this shit? What possible benefit do the moderators of superstonk get by posting this? Why are they trying so hard to stay in control of the narrative? Why do they act as if they are an authority on this topic?

The last time GameStop posted positive full-year earnings was in 2017.

There has been a fair amount of talk of GameStop posting full-year profitability for the 2023 fiscal year, which is definitely within reach, but not guaranteed.

If GameStop posts full year earnings for FY23, it will be the first time in 6 years. It will be a momentous occasion!

It will also demonstrate that the prevailing sentiment put out by mainstream media doesn't reconcile with the reality that this company is not the loser that they want the world to think it is.

sorry, correction, not ALL of the information in the chart was exclusively from that section of the 10-Q, there was also this section of the revenue:

All of the information in this diagram is derived from this section of the 10-Q:

all in all it was a decent movie.

"but it doesn't talk about [insert thing here] so therefore it was not good!"

i disagree with that notion. no such thing as bad press, and all that, and this movie isn't even bad press. it was fun and entertaining, which is typically the purpose of most movies. it was not a fact-based documentary, it's hollywood entertainment that is shining a light on an important story.

i do find it funny how much hate the movie is getting in superstonk.

In any kind of situation, sorry if I sound like a broken record here, but I always ask myself: who benefits?

We know that Public Relations is something that exists as an industry and as a component of businesses. Businesses use PR in order to shape public perception, away from something negative and sensitive to the business and towards something positive and helpful for the business.

E.g.: what did tobacco / cigarette companies do when research started coming out demonstrating that cigarettes caused cancer? Were those companies honest and forthright, and admit to this true reality even though admitting it would hurt their sales? Or did they do everything in their ability to obfuscate the truth and confuse people, because those actions led to an outcome of continued profits for the company?

We know that wall street and other industries make use of shill farms. Shill farms are basically the modern evolution of PR. If you are a wealthy and powerful incumbent and you are not using shill farms, you will fall behind and lose control of the narrative.

so, in a contest of "promote Dumb Money because it brings positive attention to GameStop", versus "Dumb Money sucks and was bad and was not good and I hated it and it didn't properly represent the story", which one of these thought processes is helpful to GME investors and which one is not?

And in consideration of that, why is it that superstonk is so loaded with antagonism towards this movie?

I think you might be right, though it is impossible to know for sure.

Like how the price started pumping a few days prior to December 6 earnings because those earnings were going to be decent and cause a positive reaction. So they get ahead of the positive reaction by preemptively pumping it beforehand for the purpose of preventing or slowing any momentum. This is what i suspect happened and may happen again in March of this year prior to earnings date.

Another kind of example of the censorship and confusion on this topic that continues to happen to this very day. It is for this reason why the subject needs to be repeatedly discussed and understood by as many GME shareholders as possible, because to this very day they continue to censor and confuse this topic to varying degrees.

January 23, 2024: a post that provides good information about the distinction between DRS and DSPP numbers gets removed from superstonk.

Even if well intentioned, posts like these ultimately are encouraging selling of shares, turning off autobuys, and sowing distrust in ComputerShare. The sources provided don’t back up these claims and how one person is interpreting this does not mean it’s fact. Please do your own due diligence when it comes to making decisions for your investment. Rule 6.

Why is this topic so contentious? Why has there been a sustained campaign to censor and confuse this specific topic, the topic of the distinction of DSPP and DRS, the fact that plan is not DRS?

Who benefits if it is crystal clear and all GME investors understand the truth? GME investors benefit. Who benefits if it is confusing and controversial and omitted (censored) from conversation? Not GME investors.

Great post. Insightful but not surprising.

From the perspective of a money-seeking billionaire like this, everything in the world is only as valuable as its measurement in dollars. Really, this type of behavior is completely normal and maybe even "smart", from the perspective of a capitalist system that rewards greed above all else.

If I am not mistaken, I also read that both Meta and Google, during the big hiring spree of 2021 / 2022, deliberately over-hired thousands of employees with no real work for them, just so that the competitors couldn't get those employees.

Imagine having so much excessive money that you can pay thousands of employees just to do nothing, simply so that your competitors might not get them.

Corporate behavior in modern capitalism is pretty fucked up. It's great if you are one of the few ultra wealthy individuals and all you care about is making more money than you even know what to do with. But beyond them, it's a ruthless and unfair system that will spit you out without a second thought, if it means some rich bastard can make even more money.

I agree!

I did start such a list but it is by no means comprehensive. Someone can take that info and expand on it :)

TLDR:

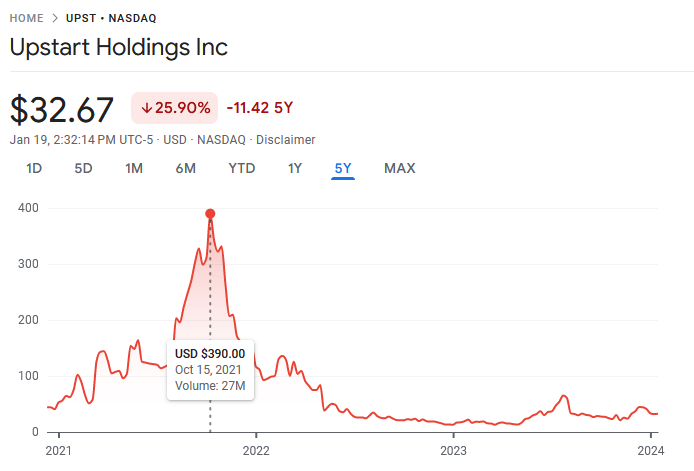

I recently saw this post and it made me curious to see how Upstart has fared since that CNBC interview was originally aired.

the original video clip appears to be from an October 15, 2021 CNBC interview with a guest by the name of Mark Minervini.

If you go to that CNBC link to view the clip, you will not find the part where Mark Minervini reveals that he has no idea what Upstart Holdings even does, this part has been conveniently removed.

Wikipedia says: "Upstart is an AI lending platform that partners with banks and credit unions to provide consumer loans using non-traditional variables, such as education and employment, to predict creditworthiness. "

By matter of pure coincidence, October 15, 2021, the same day that the original CNBC interview aired, was also the same day that Upstart Holdings was at an all time high market valuation.

So, recap:

CNBC is owned by Comcast, which is 88% owned by institutions (Wall Street)

The purpose of CNBC is the same purpose any propaganda machine.

Wikipedia provides this handy definition of propaganda, emphasis mine:

Propaganda is communication that is primarily used to influence or persuade an audience to further an agenda, which may not be objective and may be selectively presenting facts to encourage a particular synthesis or perception, or using loaded language to produce an emotional rather than a rational response to the information that is being presented. Propaganda can be found in a wide variety of different contexts.

Propaganda is the art of manipulating the perception of the target audience using a variety of lies, deceptions, and omissions of information.

It has been famously said that all warfare is based on deception.

For example in the context of a war, propaganda can be used to motivate your own troops by selling a perception of strength and success, and it can be used to demoralize your opponent's troops by selling a perception of weakness and defeat. In war, propaganda is simply a tool used to help the war-interests of the party that is utilizing the propaganda.

It's the same in the world of finance. Financial propaganda is designed to manipulate perceptions so that the person or party that is doing the manipulating may somehow benefit.

The owner of a propaganda machine like CNBC deploys the art of deception and the outcome is that the audience that consumes it subsequently hands over their hard earned money willingly and places it into the possession of that same propaganda owner.

The victim is led to believe that the information they consumed was a hot tip that might help them make some more money, but of course it was actually just a trap that took their money and gave it to Wall Street in stead.

oh man. thanks OP for reminding me of this.

I was going to leave a comment here but I am going to make a post about it in stead.

TLDR:

CNBC is financial propaganda designed to further the interests of its owners.

The owners of CNBC is Wall Street, and what Wall Street wants is more money and power for themselves and less for everybody else.

Therefore, CNBC's purpose for existence is to help Wall Street get more money and power for themselves and less for everybody else.

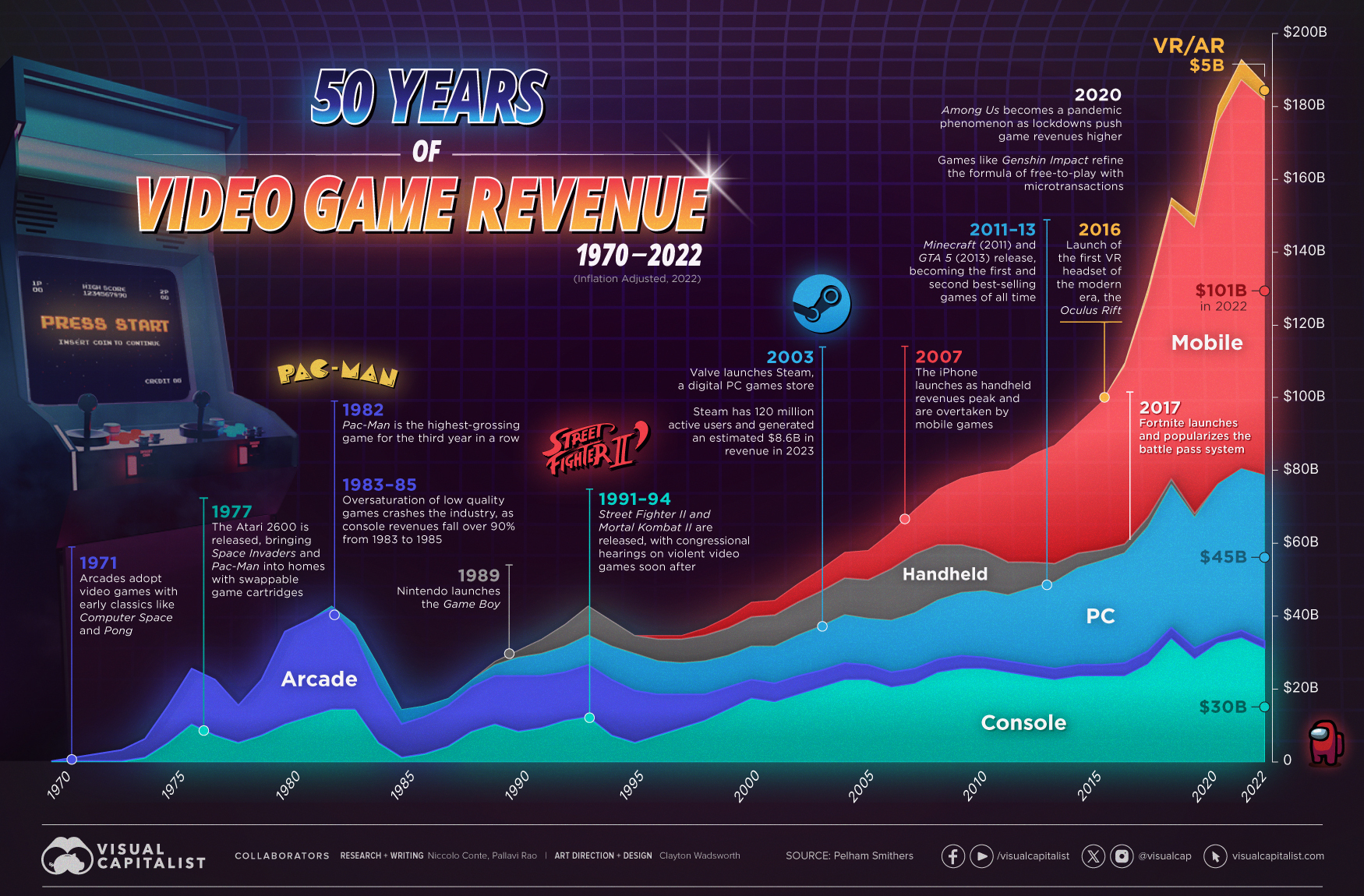

This is a December 2023 updated version of this chart which was previously posted.

This is a chart that shows information that is relevant to the interests of GME investors.

What is once again glaringly obvious is that mobile is the largest and growing area of video gaming revenue.

As it seems that GameStop is disengaging from web3 related ventures, in order to grow and succeed, GameStop will need to find reliable revenue streams.

How could a company like GameStop get a cut of that mobile gaming revenue?

"Don't forget to make sure your dividend reinvestment plan is set up again!"

Why? Why say this?

TLDR: the terms "Book" and "Plan" continue to be deliberately confused, in places of significance, and this is why it's important to continuously reiterate the simple true statement that

Somebody makes a post in superstonk that makes reference to the distinction that plan is not DRS.

In response to this, superstonk mods reply and pin to the top of that post a template message over 600 words in length that would confuse somebody who didn't know better about the plain indisputable reality that Plan is not DRS.

"Plan versus Book" is a misnomer because all electronic shares are book-entry shares. This includes Plan (aka DSPP aka DirectStock) shares and DRS shares.

It only takes 4 words to reiterate the correct truth of this distinction, the distinction being that plan is not DRS, but for some reason this is something that continues to be deliberately confused to this very day in 2024 by people that have authority over the largest online community of GME investors.

The messaging by moderators of the largest GME community has consistently been deliberately confusing and misleading, and will lead to the outcome where uninformed individuals will have an incorrect view about what is DRS and what is not DRS.

Who benefits from this?

Why do the unelected, unaccountable moderators of the largest online GME community continue to perpetrate a misleading view about something that is now so plainly indisputable?

A brief history of "plan versus book":

November 19, 2022 - Ryan Cohen tweets: "I also want to be the book king!"

"Plan versus book" enters the conscious awareness of superstonk, and thousands of people start discussing this.

Superstonk mods, slowly but surely, from Nov 2022 to January 2023, put a damper on these conversations while at the same time injecting their own several-hundred-word-deliberately-confusing message into these threads and pinning that message to the top so that everyone has to see what they want everyone to see, above what the community is talking about. "HEY OP. IT LOOKS LIKE YOU WANT TO TALK ABOUT PLAN AND BOOK. PREPARE YOURSELF FOR 600 WORDS OF PURE CONFUSION"

By January / February of 2023, threads about "plan versus book" disappear from superstonk. On odd occasion a post about this topic would come up, and get removed with a justification like "this post was removed because we already had to moderate this kind of content before!"

if the objective was to prevent further discussion of the distinction between plan shares and DRS shares, it was successful.

in April 2023, a post is made in a different subreddit, r/DRSyourGME, that re-ignites the discussion about this topic that was successfully silenced up to that point

superstonk mods tried hard to censor this topic and remove any and all mentions of what was being discussed over in r/DRSyourGME. But, their attempts at censorship failed.

uh oh.  the truth is leaking beyond superstonk's walls. Can't have that. superstonk mods publicly denounce the folks from the r/DRSyourGME subreddit and accuse them of acting inappropriately.

the truth is leaking beyond superstonk's walls. Can't have that. superstonk mods publicly denounce the folks from the r/DRSyourGME subreddit and accuse them of acting inappropriately.

Reddit decides to ban the subreddit.

June 2023 to early December 2023 - "plan versus book" once again disappears from the conscious awareness of the largest GME community.

December 2023 - in a live X spaces earnings call for GME Q3 earnings on December 6, an important conversation takes place that once again draws attention to the existence of the distinction between DRS and DSPP. It is once again re-iterated that DSPP is not DRS.

December 8: Why are DRS numbers stagnant? Exploring the possibilities ... Plan is not DRS - post by Chives

December 9: that post is then posted to r/GME

Why is this important distinction being talked about by GME investors but not in the biggest GME investor subreddit?

Apparently, the effort to continue censoring is waning. By whichever reasoning, perhaps out of the self-interested understanding that continuing to censor the topic leads to suspicion, superstonk mods relent and so graciously permit a post about this to exist.

December 22: Plan is not DRS - a post is made by jackofspades123 based on the original post by Chives.

December 22, 2023, to present: After over an entire year of this, the effort to confuse and silence discussions about the distinction between plan and DRS have failed. Censorship is no longer a viable method of information control on this topic. Time to switch gears back towards propagating and pinning a template comment that deliberately confuses the words plan and book, while continuing to ignore the important thing that plan is not DRS.

any new GME investor that is interested in DRS that gets exposed to this misleading information risks having their shares enrolled in a plan, even though what they were really seeking was DRS.

I don't necessarily know who benefits, but I know for certain that individuals seeking to inform themselves about DRS do not benefit when what they actually end up consuming is misinformation.