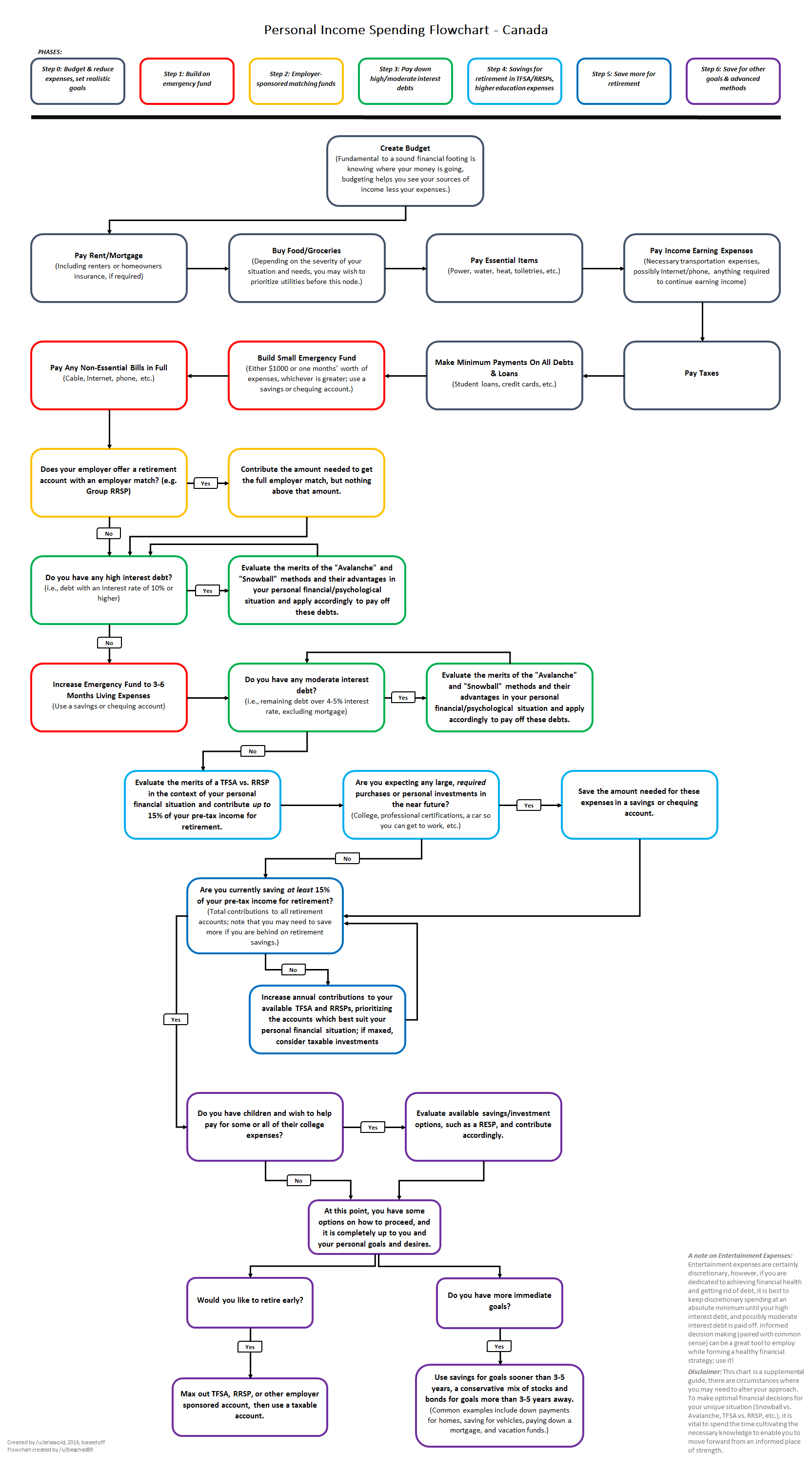

I think this chart is great, but really really complicated for someone new to this.

IMO, we should really try to work on 3 different charts : a very basic and simple one with the main steps for regular people, a standard one for people that are more interested in finance, and a hardcore one for tinkerers and optimizes...

EDIT: it should also be updated for the FHSA.