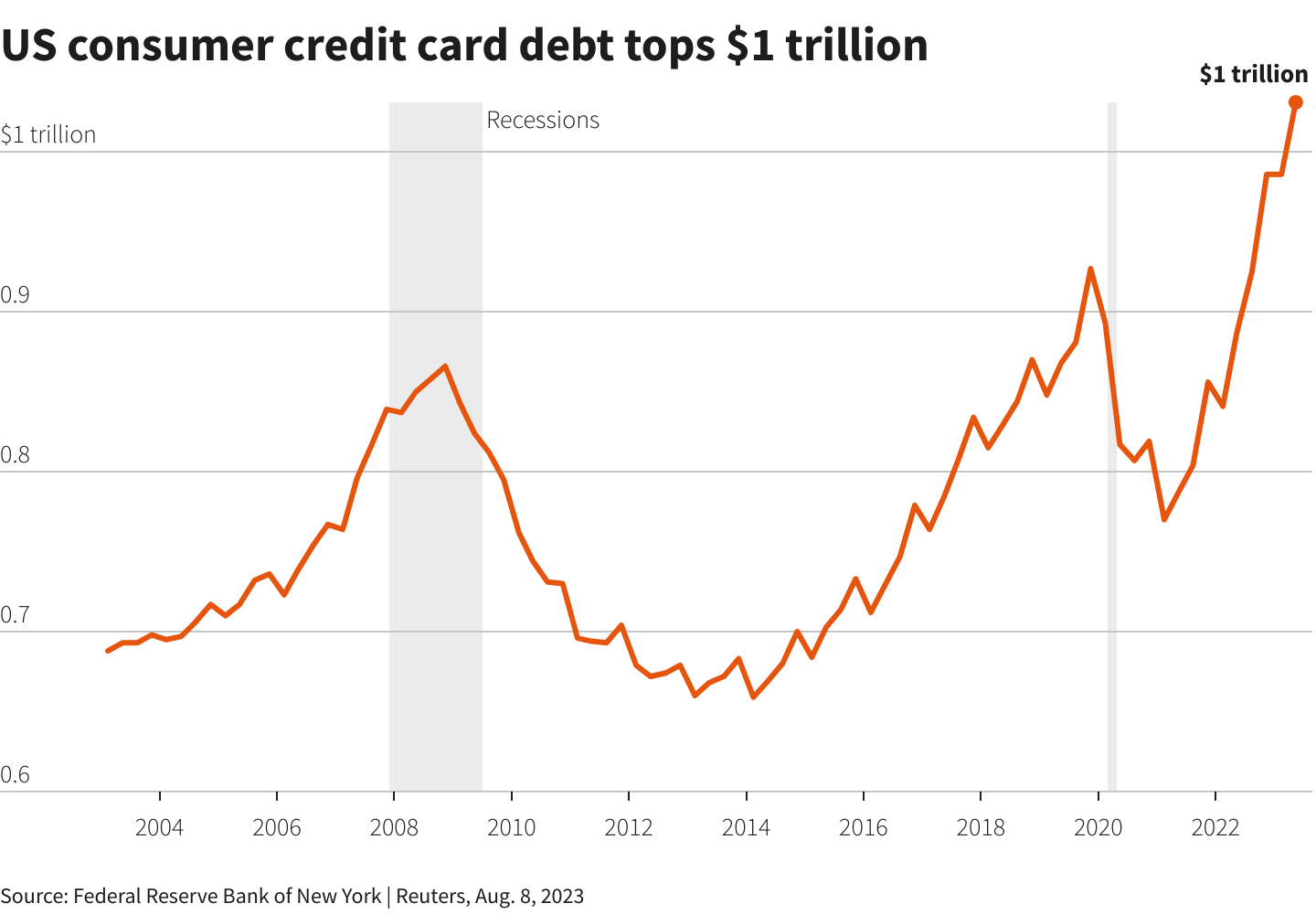

With high interest rates and inflation hitting household budgets,

goes looking for data

Hmm. This is odd. So, the article states that rates of auto repossession were higher than last year.

This says that delinquency rates on auto loans -- not quite the same thing, but probably a better sign of financial stress than repossession rate, if anything, were exceptionally high last year, according from this article in late 2023:

https://www.forbes.com/advisor/auto-loans/late-car-payments-heavy-loan-rates/

Borrowers are falling behind on car loan payments at the highest rate in 27 years. And subprime borrowers—those with credit scores below 640—are struggling the most to keep up with their monthly payments, according to the latest data from Fitch.

This graph shows that delinquency rates were low during COVID-19, but started rising after:

https://ycharts.com/indicators/us_auto_loans_delinquent_by_90_days

But this shows that loan delinquency in general, not auto loans, is up relative to the past ten years and especially relative to the very low rate during COVID-19, but if anything low over the past 30:

https://fred.stlouisfed.org/series/DRCLACBS

That'd seem to suggest that the issue is specific to auto loans, which is not really what I'd expect if interest rates and inflation are the main factors, as those should be agnostic to type of loan.

looks further

This shows that the interest rate -- nominal -- on new auto loans is high relative to the past 10 years:

https://www.statista.com/statistics/290673/auto-loan-rates-usa/

Interest rates on mortgages are high relative to the last ten years, but are about par for the course over the last thirty:

https://fred.stlouisfed.org/series/MORTGAGE30US

I'd think that things that'd tend to explain something like that would be autos being more expensive than in the past, resulting in them specifically being less-affordable. There are two data points I'd have that support that: I recall from past reading that during and after COVID-19, supply chain disruption resulted in reduced production, which resulted in higher prices for what supply was available, which resulted in used car (as a partial substitute good for new cars) prices rising. Also, the Forbes article above from October 2023 specifically says that auto prices are high (though it doesn't say whether that's in real or nominal terms):

Vehicles have also gotten more expensive. The average transaction price of a new car was $47,899 in September, down only slightly from record highs reached earlier in 2023, according to a Kelley Blue Book report. Prices for used cars also remain high, after being driven up dramatically amid supply chain snags in the new car market during the pandemic.

EDIT: Oh, I think I know part of what's going on. The bit above isn't saying that auto delinquency rates are the highest they've been in 27 years. They're saying that they're increasing at the fastest rate that they have in the past 27 years, which is more-understandable, coming off of a period of low interest rates to high interest rates.